Fertilizer

Manufacturers shoot themselves in the foot Fertilizer

Manufacturers shoot themselves in the foot

The fertilizer

industry is not a freely competitive business as we know.

Their April 1,

2022 prices are only about 93 cents for NH3, 82-0-0 at 1 pound N.

While Solution 32-2-0 is about 15% more at $1.11 per lb of N ģ.and

urea, 46-0-0 is 11 per cent more at $1.04 per lb of N.

Confirming the

differences should be 150% difference between 32-0-0 and NH3 Nitrogen.

Recent information means is not so recent in your lifetimeģwhen

Natural Gas prices stay lowģ.and why would Nitrogen..jump so

muchģ.Oligarchyģ.CF, Koch and Nutrien. Koch being the worst.

Our false economy

is simpleģit is a shell game. The cost to build NH3 at Dodge City

Kansas varies between 65 dollars to 200 dollars per ton. Which 3.6

cents to 12 cents per lb of Nģthe markup is 8 times and more. At

$1,650 per ton in Iowa.

Here is another

goofy scenarioģ.it cost too much to raise corn and wheatģ.so soybeans

lead the wayģ

USDA: Soybean acres to surpass

corn for third time ever

Getty/iStockphoto/bernardbodo

2022 corn acreage falls 4% from last

year, while all-wheat acres inch 1% higher

Ben Potter | Mar 31, 2022

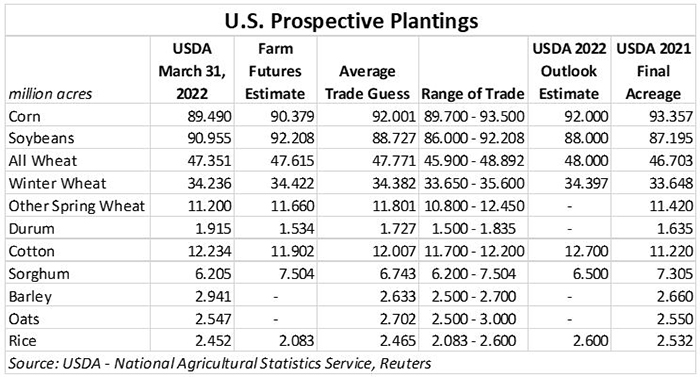

For only the third time in U.S. history,

farmers are going to plant more soybeans than corn in 2022. USDAÆs

prospective plantings report found soybean acreage will rise 4%

from last year to 90.955 million acres ¢ beating the previous

record high set in 2017 of 90.2 million acres. The cut to corn

acreage will result in a combined corn and soybean planted acreage

of 180.4 million acres, just a hair behind last yearÆs

record-setting high of 180.6 million acres.

High input costs, especially in regions

outside of the Corn Belt, likely contributed to the acreage

switch. As early as January, Farm Futures predicted

soybean acres would eclipse corn acres for only the third time

on record, thanks to input and analysis from our exclusive grower

surveys.

Acre swap

Related:

Dig into the latest USDA report

USDA estimates that corn plantings

will tilt 4% lower this year, to 89.5 million acres, which is

nearly 4 million acres lower (3.87 million) compared to 2021.

Versus a year ago, planted acres are expected to hold steady or

drop in 43 of the 48 estimating states.

ōGrowers are expected to plant 3.9

million fewer acres of corn,ö notes Farm Futures grain market

analyst Jacqueline Holland. ōThe 2022 projection of 89.5 million

corn acres will be the smallest corn crop since farmers planted

88.9 million acres in 2018. Assuming trendline yields of 181.0

bushels per acre, the 2022 crop could rise to 14.8 billion bushels

¢ the third largest corn crop in U.S. history.ö

ōFarm FuturesÆ balance sheet calculations

project a conservative 2022/23 corn stocks-to-use ratio of 8.6%, which

if realized will be the seventh tightest U.S. corn supply on record,ö

Holland continues. ōThat bullish prospect fueled Chicago Board of

Trade corn futures prices for 2022 crop contracts to 3.5%-4.3% gains

in the reportÆs aftermath.ö

Soybean acres of just below 91.0 million

acres will be a record-breaking effort, if realized. Twenty-four of

the reporting 29 states are expected to hold steady or increase acres

this year.

ōA record soybean sowing will inevitably

lead to a record soybean crop if trendline yields are realized this

year,ö Holland says. ōAt 90.2 million acres and 51.5 bpa yields, the

2022 soybean crop will eclipse last yearÆs high (4.4B bu.) to a

record-setting 4.6 billion bushels.ö

But amid South American crop shortfalls,

tight global edible oil supplies, and an expanding biodiesel industry

at home, the extra bushels wonÆt completely eliminate supply worries,

Holland adds.

ōEven though soybean prices fell after

the reportÆs release, the 2022/23 soybean stocks-to-use ratio is only

projected by Farm Futures to rise 1.7% to 8.2% ¢ the 25th

tightest soybean supply on record,ö she says. ōAs our team predicted,

soaring input costs will limit upward acreage expansion. USDAÆs cuts

to 2022 spring wheat reaffirmed that estimation with its 5% annual cut

to 2022 spring wheat acreage, leaving it at 11.2 million acres for the

year.ö

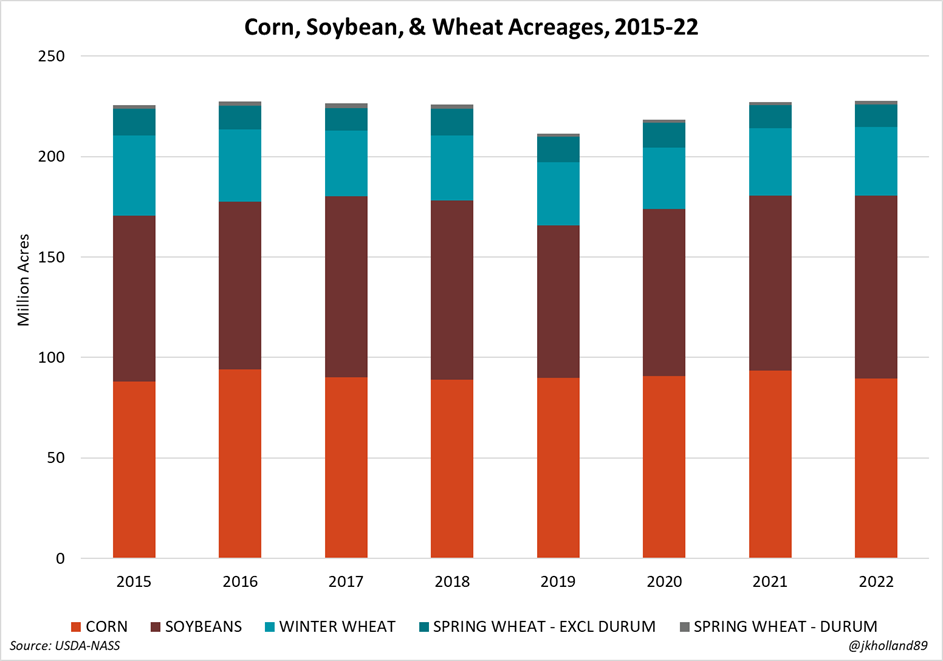

All-wheat acres should rise 1% from a

year ago to 47.4 million acres. That includes 34.2 million acres of

winter wheat acres (up 2% from 2021) and another 11.2 million acres of

spring wheat (down 2% from 2021). Durum acres are expected to jump 17%

from a year ago to 1.92 million acres.

ōUSDA slightly trimmed previous estimates

for winter wheat acreage, though total planted wheat acreage is

expected to rise to 47.4 million acres ¢ a four-year high,ö Holland

says. ōThat will add some breathing room to 2022/23 U.S. wheat stocks,

especially if feed usage creeps lower and global buyers find

alternative ¢ and cheaper ¢ substitutes for Black Sea wheat.ö

Wheat futures largely had these

sentiments priced in prior to the reportÆs release, though the spring

and winter wheat acreage cuts most benefited Kansas City hard red

winter wheat and Minneapolis spring wheat futures, Holland adds.

That leaves combined acres for corn,

soybeans and wheat at 227.8 million acres. Holland says thatÆs the

seventh-largest combined footprint for the three crops, surpassing

last yearÆs total by 541,000 acres amid rising soybean and winter

wheat plantings.

With strong cotton prices, acres for that

crop is expected to climb 9% higher year-over-year to 12.2 million

acres. Upland accounts for the vast majority of those plantings, with

12.1 million acres ¢ but American Pima could trend 39% higher from a

year ago, to 176,000 acres.

No stock shocks

ōThere really werenÆt any surprises on

the Quarterly Grain Stocks side of todayÆs reports,ö according to

Holland.

For corn, the agency shows corn stocks

tumbling from 11.647 billion bushels in December down to 7.850 billion

bushels in March. That was also slightly below the average trade guess

of 7.877 billion bushels but a bit above year-ago results of 7.696

billion bushels.

Soybean stocks followed a similar path,

dropping from 3.149 billion bushels in December down to 1.931 billion

bushels in March ¢ staying moderately above year-ago totals of 1.562

billion bushels. Analysts generally expected to see smaller quarterly

stocks, with an average trade guess of 1.902 billion bushels.

Wheat quarterly stocks trended from 1.390

billion bushels in December down to 1.025 billion bushels in March.

Unlike corn and soybean stocks, that total was moderately lower than

year-ago results of 1.311 million bushels. It was also lower than the

average trade guess of 1.045 billion bushels.

ōWe knew coming into the reports that

wheat supplies were going to be low because of last yearÆs spring

wheat crop shortfalls,ö Holland says. ōBut we are also starting to see

some diminished usage as high prices create buying resistance. Plus,

USDA had already indicated in the March 2022 World Agricultural Supply

and Demand Estimates report that wheat growers have already sold most

of their 2021 wheat crops.ö

Green Play AmmoniaÖ, Yielder« NFuel Energy.

Spokane, Washington. 99212

www.exactrix.com

509 995 1879 cell, Pacific.

Nathan1@greenplayammonia.com

exactrix@exactrix.com

|